Debt is essential. Some financial professionals say, “Never go into debt.”. Those professionals would be correct, stay out of bad debt. There is a time when debt is critical to wealth development. Debt can be used to leverage the dollars you have to create great wealth and cash flow. Now I’m not telling you to leverage every dollar you have in the “hopes” of getting wealthy quickly. That isn’t very intelligent. But what I am an advocate for is smart uses of debt.

So when is debt appropriate and valuable? It’s when you can afford it. If it were that simple, this would be the end of this post. To afford debt is if you can make the debt service/payment. I say debt service because some debts have different terms. Such as interest only or a balloon payment. Understanding the terms of debt is essential to know how much you have to service.

After working in finance, I’ve realized that people don’t know how to calculate their discretionary income or understand how payments are calculated.

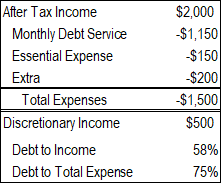

Your discretionary income is your income after all your necessary expenses. I emphasize necessary expenses because Netflix and Spotify are not essential to your survival. (You can argue with me all you want.) Your essential expenses include rent or mortgage, utility bills, and other monthly debt obligations. In finance, we use the ratio of debt to income to calculate the riskiness of a potential client. It would be highly beneficial for you to know how to calculate it. Start with your after-tax income, divided by your monthly debt obligations. For example, let’s say someone makes $2,000 and has $800 rent, a $300 car payment, and a $50 minimum due on their credit card. The debt to income would be 58%. ($800+$300+$50/$2000=58%). In finance, we would like to see this ratio below 50% better if it was in the 30% to 40% range. Someone at 50%, meaning that half of their income goes to debt obligations, is rather risky.

This would not be a personal financial Substack if I didn’t provide something that could help you on your journey to financial freedom. So we know that banks use debt-to-income ratio, but here’s something that you can track on your own that the banks don’t, and if this ratio is good, then your debt-to-income will be even better. I call this ratio - total expense to income. It combines your monthly debt obligation with your necessary expenses, utility bills, and non-essential expenses like Netflix and Spotify. To build upon the above example, now account for $150 in essential expenses with $200 in extra spending. Look at the chart below to see how adding the essential and non-essential expenses to the equation affects the ratio.

We just learned that banks look at debt to income. In the example above, a bank could give a loan to someone with 58% debt to income but see how a mistake can be made if someone truly can’t afford any additional debt if their debt to total expenses is high. In the example above, this person only had 15% of their income or $500 to take on any new obligations. They could lower this ratio by cutting their extra spending or increasing their income. Even more, problems can happen if this person doesn’t understand the debt terms fully on their existing debt obligations. Examples of this could be adjustable rates or balloon payments.

In conclusion, understanding how much debt you can afford is the first step in understanding why debt is essential. The following posts will examine how debt can be utilized to purchase cash-flowing assets.

Debt shouldn’t be feared; it should be respected.

Remember, this is not financial advice; just how I see things as a financial professional. If you found this helpful, you can pay me a favor and share it with someone or send me a funny meme in the comments.